Introduction. Everyone knows that the most famous coin in the world is Bitcoin. Satoshi Nakamoto is the founder of Bitcoin. there are so many popular networks working recently. many to come. bep20, erc20, polygon, Solana, Tron networks are some of them. The auto-staking protocol is a very powerful protocol that allows people to stake their tokens more easily and quickly. The auto-staking platform uses a mechanism where users don't have to bother to stake their tokens. Later users will be able to stake their tokens without the need to manually stake, the system will automatically reward users for the tokens they hold. The more tokens a user has, the bigger the reward they will get. And all of that will be able to be monitored by users directly on their growth in their digital wallet. This is why staking platforms with auto-staking protocols are a favorite of today's users as they don't have to bother with their token stakes and just need to last ...

Dapatkan link

Facebook

X

Pinterest

Email

Aplikasi Lainnya

HADA DBANK - AI analysis and blockchain technology create an ethically and globally responsible banking

HADA DBANK

Hada DBank is the first digital bank to combine sharia banking module with blockchain technology to create an ethical and responsible banking ecosystem. Existing players make money out of debt and interest. This is why the global economy has collapsed from time to time since the first century. Hada DBank chose to be part of the financial revolution through the creation of a caring and personal bank. this is the core value of Hada DBank that forms and influences services, transactions, interactions and runs the banking business. We aspire to improve people’s lives. Personalization will be the main focus in Hada DBank’s services. Different customers have different needs, and require different services and attention. DBA’s HADA customers will have customized services. Banks learn from the effects of the trap of modern financial institutions, and choose Islamic banking for the future. The principles of Sharia banking require total transparency from customers and banks. Conscientious decision making, backed by market insight, real digital analysis, AI analysis and blockchain technology will no doubt benefit customers. Hada DBank promotes ethical and globally responsible banking. Syariah banking is not just for Muslims but for everyone. But it does represent “Transparency and Risk Sharing”. real digital analysis, AI analysis and blockchain technology will undoubtedly benefit customers. Hada DBank promotes ethical and globally responsible banking. Syariah banking is not just for Muslims but for everyone. But it does represent “Transparency and Risk Sharing”. real digital analysis, AI analysis and blockchain technology will undoubtedly benefit customers. Hada DBank promotes ethical and globally responsible banking. Syariah banking is not just for Muslims but for everyone. But it does represent “Transparency and Risk Sharing”.

Mission Providing ethical and responsible banking services to all people, especially the current “Unbanked” population

Vision Being the leader of global blockchains & digital banks that emphasize ethics and responsibility through the principles and services of sharia banking

We have bad experiences with conventional banks either because of high service fees or lack of empathy during transactions with their personnel. In HADA DBANK developed a comprehensive digital blockchain bank that will make life easier for everyone. They will be able to perform banking activities at a cost of 0% and at the same time enjoy the quality of service from us. We are here not just for profit, but to make a fair profit and ensure a better banking experience. HADA DBANK will become a blockchain-based digital bank in the world by integrating sharia banking model with blockchain technology, to create an ethical and responsible banking ecosystem. We chose to win Islamic banking services using pre-ICO funds to apply for FinTech License from Swiss FINMA. An application for the Start-Up Unit of a new bank license will be applied with the Prudential Bank of England’s financial authorities and regulations.

WHY IS ISLAMIC BANKING? Our reason is simple. We aspire to be a ‘fair’ organization in the financial industry. The financial crisis of 2007–2008 serves as a reminder of how some irresponsible players can reverse the whole industry.

Sharia banking with its transparency system, its advantages and disadvantages with the profit sharing concept, will minimize market manipulation and eliminate other domino crashes. Islamic banks are less risky and tougher than conventional banks. The depositors to sharia banks are entitled to information about what banks do with their money.

They also have a vote where their money should be invested. Islamic banks also seek to avoid interest at all levels of financial transactions and promote risk sharing between lenders and borrowers. There are two basic principles in sharia banking, namely the distribution of the advantages and the prohibition of interest collection and payment by creditors and investors. Collecting interest or “Riba” is not permitted under Islamic law. In terms of profit, the bank and the customer in the proportion that has been agreed previously. In case of loss, all financial losses will be borne by the lender. In addition, Islamic banks can not create debt without goods and services to support it (ie physical assets including machinery, equipment, and inventory). Therefore savings, deposits and investments with Hada DBank will be supported by physical assets such as precious metals and gemstones. Demand for Islamic banking is enormous. There are 1.7 billion Muslims worldwide, and this number is growing.

HADA DBANK provides alternative financial services to all consumers and investors. The recent global financial crisis shows the resilience of sharia banking and the financial industry. In 2008–2009, the Islamic banking industry is estimated to have experienced asset growth compared to the conventional banking sector. You may think that Islamic banking is only for Muslims. in June 2014, Britain became the first non-Muslim country to issue Sukuk. Islam is equivalent to a bond (the word itself is the plural of Sakk, meaning contract or deed). In September 2014, the governments of Luxembourg and South Africa as well as the Hong Kong Monetary Authority made the publication. But the Sukuk is not limited to the ruler. In September 2014, Goldman Sachs issued a Sukuk of USD500 million and Bank of Tokyo-Mitsubishi Malaysia raised the first USD50 from the issuance of USD500 million. All these entities in Islamic financial markets amount to USD2 Trillion. Regardless of the Muslim population of 1.7 Billion and billions of others who prefer to subscribe to Islamic banking services, HADA DBANK will also focus on populations of 644.1 million residents of Southeast Asia (ASEAN). Interesting facts about ASEAN: 7 Billion and billions of others who prefer to subscribe to Islamic banking services, HADA DBANK will also focus on population of 644.1 million people of Southeast Asia (ASEAN). Interesting facts about ASEAN: 7 Billion and billions of others who prefer to subscribe to Islamic banking services, HADA DBANK will also focus on population of 644.1 million people of Southeast Asia (ASEAN).

Interesting facts about ASEAN:

Have a population that has no banking I about 438 million.

More than half of the ASEAN population is under 30 years of age.

Have a market penetration of 854 million smartphones or 133% compared to the population, but only 53% of ASEAN population online, leaving significant space for market expansion in Indonesia. As an online specialty bank, this fact convinces us to focus on ASEAN as our secondary market. We are scheduled to offer Hada DBank Syariah Banking Services offered gradually in the second quarter of 2018.

Features and Benefits of Hada Bank Encrypted free account & e-Wallet

Savings & Withdrawals a. Minimum 5% return on savings per year b. No withdrawal fees

Transfer, Remittance & Exchange a. free transfer and remittance fees (fiat and cryptocurrency) between personal storage account and e-wallet b. minimum 0% fee on exchange transactions via HADA Exchange (between crytocurrency). There is no charge on the primary FIAT currency during crypto currency-fiat exchanges. c. Connect with partners or open the API to get better interest rates for other currencies 4.Loan & Investment a. 0% Loan Interest b. 10% minimum investment return

Real-Time Payments Real-Time Payments use HADACoin and Cryptocurrencies / Tokens through our Debit Card BOT HADA Financial Management Bot / Personal Finance Assistant (HUDA) Helps you in managing your daily or monthly expenses by showing your daily expenses & limits, either set by you or your account balance. Remind you of bills, suggest and pay them accordingly, through prioritized scheduled based on your account balance (your savings or even your e-Wallet). Short-term financial goals, for example, help you save for the holidays you want. Long-term financial goals, such as saving for a dream wedding or your early retirement plan.

AI (Artificial Intelligence) Personal Financial Advisor (HADI) helps you invest by providing impartial financial advice

Cashback & Discount Money change and discounts are paid when using a debit card for the first year. Extra change and discount if using HadaCoin forever. Get additional discounts from partners and affiliates.

Bonus and Bounty

System points

Collect points from your expenses with e-Wallet or Debit Card and convert into cash or cryptocurrency / token. Use additional discounts to pay for whatever you want and save more on your purchase. You can also use points collected to redeem anything you like in partner e-malls or physical outlets around the world.

Increase capital for DBADK HADA development through HADACoi used for banking transactions or daily activities. Customers are given a debit card that enables them to trade with HADACoin in the HADA banking platform or any other merchant globally.

As many as 500 million HadaCoins will be issued. 295 million coins will be offered for sale. Of the 295 million coins, 20 million will be allocated to private investors and institutional buyers, 50 million coins will be released during PRA-ICO exercises and the remaining 225 million coins will be released in our ICO practice in the near future. 10 million coins will be allocated to the bonti campaign.

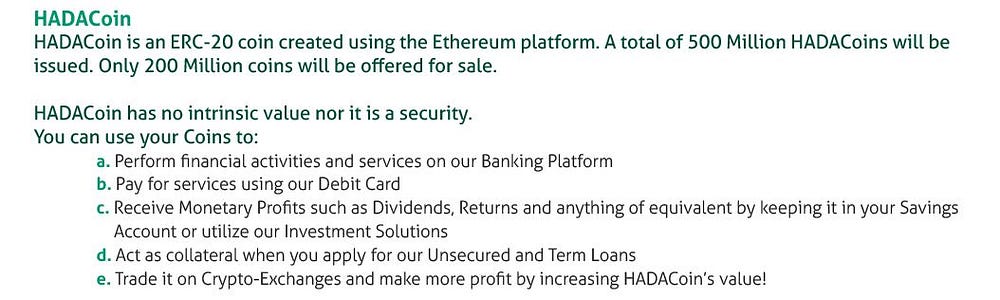

HADACoin is an ERC-20 coin made using Ethereum platform. A total of 500 million HadaCoins were created. HADACoin has no intrinsic value and no security, no guaranteed monetary gains such as dividends, returns or related when buying coins. You can use coins to perform activities and financial services on the banking platform Hada DBank, pay by debit card, receive monetary benefits or take advantage of investment solutions, as collateral for unsecured loan applications, market it in Crypto-Exchanges and generate more profits by increasing the value HADACoin.

The 35% capital earned through PRE-ICO is allocated for research & development. Among them are offices, hardware investments for developer departments, business assets, and precious metals and precious stones (gold, silver and diamonds), to be used as collateral for future savings, investments and HADACoin value. The last 15% will be saved as RESERVE. This reserve will not be used unless it is needed and strict rules will be established. The decision to utilize this reserve will be determined by top management collectively and unanimously, to ensure no mismanagement and excess reserve use. We will increase DBADK’s HADA reserves to 30% of total capital in accordance with Islamic Finance Law

HADA DBANK uses private blockchain stored in every node in the network controlled by DBANK HADA. Some nodes only store a blockchain copy and can act as a gateway node or server backup node that acts as a validator on a secure network. This feature ensures the ability to validate database and transaction history anytime in the future. The primary database stores all the data that passes its core. In addition to the main database, there are other databases that store only the final state of the core. This database is optimized for rapid read and write account data during new transaction validation. Thus, each node in the network stores and processes the core state using two databases simultaneously to search and read transaction data quickly, others support history and general synchronization with other nodes in the network. The DBANK HADA architecture consists of different components in which each component handles a set of separate functions. To modify each component independently by adding new features, as well as designing and launching new platform components. In terms of geographic location, components can be in permanent or non permanent places. The interaction between platform components is done through a message or a request exchange, which is broadcast over a network channel. The method for building these channels depends on the type of components and safety requirements. In addition, the platform is a rule for authentication between components. The DBANK HADA architecture consists of different components in which each component handles a set of separate functions. To modify each component independently by adding new features, as well as designing and launching new platform components. In terms of geographic location, components can be in permanent or non permanent places. The interaction between platform components is done through a message or a request exchange, which is broadcast over a network channel. The method for building these channels depends on the type of components and safety requirements. In addition, the platform is a rule for authentication between components. The DBANK HADA architecture consists of different components in which each component handles a set of separate functions. To modify each component independently by adding new features, as well as designing and launching new platform components. In terms of geographic location, components can be in permanent or non permanent places. The interaction between platform components is done through a message or a request exchange, which is broadcast over a network channel. The method for building these channels depends on the type of components and safety requirements. In addition, the platform is a rule for authentication between components. In terms of geographic location, components can be in permanent or non permanent places. The interaction between platform components is done through a message or a request exchange, which is broadcast over a network channel. The method for building these channels depends on the type of components and safety requirements. In addition, the platform is a rule for authentication between components. In terms of geographic location, components can be in permanent or non permanent places. The interaction between platform components is done through a message or a request exchange, which is broadcast over a network channel. The method for building these channels depends on the type of components and safety requirements. In addition, the platform is a rule for authentication between components.

Decentralized computer networks validate and confirm transactions under DBANK HADA control using specially developed software. Exchanging information between network nodes is done using an isolated network from the internet. Every computer in a decentralized network keeps the core and history of all transactions done. Any transaction that is authenticated by its core can not be changed as it is stored in chronological order in blockchain. Conducting banking activities is very difficult with conventional methods that include visiting branches or ATMs that are limited in number and location and online banking can be a hassle to unbanked. “Normal” banking activity becomes a tedious and intimidating process for the uneducated. Therefore, we created DBANK HAD with the intention to make it easier for everyone to do banking activities regardless of their social status. We believe we have the technology. Anywhere HADA DBANK will issue a prepaid debit card. This prepaid debit card will enable customers to “unbanked” cashless transactions. They are not required to have a bank account or e-Wallet with us to enjoy this service. Customers can also withdraw and cashback through any partnering with ATMs and merchants globally. There are no service fees and withdrawals for customers to enjoy this service. HADA DBANK will enforce strict KYC procedures to deter fraud and money laundering.

HADACoin

Pre-ICO will begin 16 Nov 2017 (00:00 EST) and Ends 17 Dec 2017 (00:00 EST). Pricing of the Pre-ICO is:

1 Ethereum= 800 HADACoins including 25% Bonus (1st Week)

1 Ethereum= 700 HADACoins including 20% Bonus (2nd Week)

1 Ethereum= 600 HADACoins including 15% Bonus (3rd Week)

1 Ethereum= 500 HADACoins including 10% Bonus (4th Week)

1 Ethereum= 400 HADACoins (5th Week +)

ICO

A full ICO will be launched in the 1st Quarter of 2018 (target: March). HADA DBank will distribute the remaining 150 Million coins during the ICO exercise.

TEAM

Conclusions and References

We aspire to be a just organization in the financial industry. The financial crisis of 2007-2008 serves as a grim reminder how several irresponsible players can capsize an entire industry, putting millions in financial ruins. Islamic banking, due to its transparency, profit and loss sharing concept, will minimize market manipulation and eliminate another domino crash. Islamic Banks are less risky and more resilient than their counterparts, due to the aspects of their bank capital requirements and mobilisation of deposits. As opposed to Conventional Banking, depositors to Islamic Banks are entitled to be informed about what the bank does with their money. They also have a say in where their money should be invested. Islamic banks also strive to avoid interest at all levels of financial transactions and promote risk-sharing between the lender and borrower. There are two basic principles in Islamic banking. One is the sharing of profit and loss; and two, significantly, the prohibition of the collection and payment of interest by lenders and investors. Collecting interest or “Riba” is not permitted under Islamic law. In the case of profit, both the bank and its customer share in a pre-agreed proportion. In the case of a loss, all financial losses will then be borne by the lender. In addition to this, Islamic bank cannot create debt without goods and services to back it (i.e. physical assets including machinery, equipment, and inventory). Hence savings, deposits and investments with our DBank will be backed by physical assets such as precious metals and gemstones.

For more information for reference, please visit the following link:

Komentar

Posting Komentar